Reverse acquisitions (reverse mergers) present unique accounting and reporting considerations. Depending on the facts and circumstances, these transactions can be asset acquisitions, capital transactions, or business combinations. See BCG 7.1.2 for further information on the accounting for when a new parent is created for an existing entity or group of entities. A reverse acquisition that is a business combination can occur only if the accounting acquiree meets the definition of a business under ASC 805. An entity that is a reporting entity, but not a legal entity, could be considered the accounting acquirer in a reverse acquisition. Like other business combinations, reverse acquisitions must be accounted for using the acquisition method.

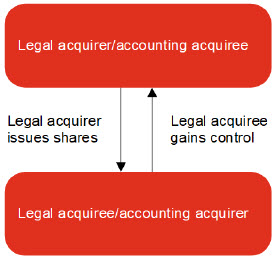

A reverse acquisition occurs if the entity that issues securities (the legal acquirer) is identified as the acquiree for accounting purposes and the entity whose equity interests are acquired (legal acquiree) is the acquirer for accounting purposes. For example, a private company wishes to go public but wants to avoid the costs and time associated with a public offering. The private company arranges to be legally acquired by a publicly listed company that is a business. However, after the transaction, the owners of the private company will have obtained control of the public company and would be identified as the accounting acquirer under ASC 805. In this case, the public company would be the legal acquirer, but the private company would be the accounting acquirer. The evaluation of the accounting acquirer should include a qualitative and quantitative analysis of the factors. See BCG 2.3 for further information. Figure BCG 2-1 provides a diagram of a reverse acquisition.

Figure BCG 2-1

The legal acquirer is the surviving legal entity in a reverse acquisition and continues to issue financial statements. The financial statements are generally in the name of the legal acquiree because the legal acquirer often adopts the name of the legal acquiree. In the absence of a change in name, the financial statements remain labelled as those of the surviving legal entity. Although the surviving legal entity may continue, the financial reporting will reflect the accounting from the perspective of the accounting acquirer, except for the legal capital, which is retroactively adjusted to reflect the capital of the legal acquirer (accounting acquiree) in accordance with ASC 805-40-45-1.

The merger of a private operating entity into a nonoperating public shell corporation with nominal net assets typically results in (1) the owners of the private entity gaining control over the combined entity after the transaction, and (2) the shareholders of the former public shell corporation continuing only as passive investors. This transaction is usually not considered a business combination because the accounting acquiree, the nonoperating public shell corporation, does not meet the definition of a business under ASC 805. Instead, these types of transactions are considered to be capital transactions of the legal acquiree and are equivalent to the issuance of shares by the private entity for the net monetary assets of the public shell corporation accompanied by a recapitalization.

Any excess of the fair value of the shares issued by the private entity over the value of the net monetary assets of the public shell corporation is recognized as a reduction to equity.

In a reverse acquisition, the accounting acquirer usually issues no consideration for the acquiree. Instead, the accounting acquiree usually issues its equity shares to the owners of the accounting acquirer. Accordingly, the acquisition-date fair value of the consideration transferred by the accounting acquirer for its interest in the accounting acquiree is based on the number of equity interests the legal subsidiary would have had to issue to give the owners of the legal parent the same percentage equity interest in the combined entity that results from the reverse acquisition.

In a reverse acquisition involving two public companies, there is a reliably measurable market value for the common stock of both entities. Accordingly, the acquisition-date fair value of the shares of the accounting acquirer should be used to measure the consideration transferred. The consideration transferred is determined based on the number of shares the accounting acquirer would have had to issue to the shareholders of the legal acquirer to achieve the same ownership ratio in the combined entity (i.e., give the shareholders of the legal acquirer the same percentage of equity interests in the combined entity that results from the reverse acquisition).

In a reverse acquisition involving only the exchange of equity, the fair value of the equity of the accounting acquiree may be used to measure consideration transferred if the value of the accounting acquiree’s equity interests is more reliably measurable than the value of the accounting acquirer’s equity interest. This may occur if a private company arranges to be legally acquired by a public company with a quoted and reliable market price, and the owners of the private company will control the public company such that the private company is identified as the accounting acquirer under ASC 805. If so, the accounting acquirer should determine the amount of goodwill by using the acquisition-date fair value of the accounting acquiree’s equity interests in accordance with ASC 805-30-30-2 through ASC 805-30-30-3.

Example BCG 2-38 illustrates the measurement of the consideration transferred in a reverse acquisition.

EXAMPLE BCG 2-38

Valuing consideration transferred in a reverse acquisition (adapted from ASC 805-40-55-8 through ASC 805-40-55-10)

Company B, a private company, is the accounting acquirer of Company A, a public company, in a reverse acquisition. The transaction is a business combination.

Immediately before the acquisition date:The fair value of the consideration effectively transferred should be measured based on the most reliable measure. Because Company B is a private company, the fair value of Company A’s shares is likely more reliably measurable. Assuming that Company A’s fair value is more reliably measurable, the consideration effectively transferred would be measured using the market price of Company A’s shares ($16/share) multiplied by the number of shares owned by Company A shareholders of the newly combined entity (100 shares) or $1,600.

If the fair value of Company B’s shares were more reliably measurable, the fair value of the consideration effectively transferred would be calculated using the amount of Company B’s shares that would have been issued to the shareholders of Company A on the acquisition date to give Company A an equivalent ownership interest in Company B as it has in the combined company. Company B would have had to issue 40 shares 1 to Company A shareholders, increasing Company B’s outstanding shares to 100 shares. Consideration effectively transferred would be $1,600 (40 shares times the fair value of Company B’s shares of $40).

An acquirer in a business combination may agree to exchange share-based payment awards held by grantees of the acquiree for replacement share-based payment awards of the acquirer. The accounting acquirer should apply acquisition accounting to the business combination regardless of the legal form of the transaction. In a reverse acquisition, from a legal perspective, outstanding share-based payment awards held by the grantees of the legal acquirer have not changed. However, from an accounting perspective, the awards have been exchanged for share-based payment awards of the accounting acquirer (legal acquiree). Accordingly, the acquisition-date fair value of the legal acquirer’s (accounting acquiree’s) share-based payment awards need to be evaluated to determine whether the awards should be included as part of the consideration transferred by the accounting acquirer or should be recognized as compensation cost in the accounting acquirer’s postcombination financial statements. See BCG 3.2 for detail on determining whether compensation arrangements represent compensation for (1) precombination vesting (i.e., part of the consideration transferred), (2) postcombination vesting (i.e., accounted for separate from the business combination as costs in the postcombination period), or (3) a combination of precombination and postcombination vesting.

For any share-based payment awards held by the grantees of the accounting acquirer (legal acquiree), the legal exchange of the accounting acquirer’s awards for legal acquirer’s awards is considered to be a modification under ASC 718 of the accounting acquirer’s outstanding awards. See SC 4 for further guidance on the accounting for modifications.